This article is published in Aviation Week & Space Technology and is free to read until Sep 05, 2024. If you want to read more articles from this publication, please click the link to subscribe.

Keys To Better Airline Margins Are Consolidation And Government Policy

IATA published improved airline industry profit forecasts for 2024 during its Annual General Meeting in June and also upwardly revised its 2023 estimates. This is the result of strong demand, still benefitting from the post-COVID overhang of consumer enthusiasm for flying. This is driving revenue growth faster than cost growth, according to IATA.

IATA now expects the world airline industry to generate a net profit of $30.5 billion in 2024, up from $27.4 billion in 2023. This would be the highest number since 2017. In its last industry outlook, published in December 2023, IATA had forecast $25.7 billion for 2024, up from $23.3 billion in 2023.

However, margins remain thin—the net profit margin is expected to be just 3.1%—and the industry remains unable to generate a return on capital that meets its cost of capital. As post-pandemic pent-up demand starts to soften, generating a sufficient return will become yet more challenging.

This further supports CAPA’s view that airline industry structure must change in the direction of greater consolidation to drive returns up. This will require policy changes from governments and regulators.

IATA’s 2024 forecasts confirm that the world airline industry is expected to perform better than in 2019 on almost every important measure. It can be calculated from IATA’s forecasts and historic data that scheduled passenger numbers are set to be up by 9% compared with 2019, RPKs up by 5%, and cargo volume up by 1%.

None of these traffic measures exceeded 2019 levels in 2023. However, passenger yield has been above 2019 since 2022, and cargo yield has been higher than pre-pandemic levels every year since 2020 (although it has fallen from its 2022 peak).

Passenger yield and cargo yield are both forecast to be 17% above 2019 levels in 2024. Passenger revenue is expected to exceed 2019 by 23%, cargo revenue by 19%, other revenue by 2%, with total revenue up by 19% over 2019 in 2024.

Net profit is forecast to be 16% higher than in 2019. The net margin is forecast to be 3.1%, the same as in 2019, but the operating profit margin is forecast to be up by 0.8 percentage points, to 6.0%.

A further measure favored by IATA is net profit per departing passenger. This is forecast to be $6.14 in 2024, which is 6% higher than in 2019.

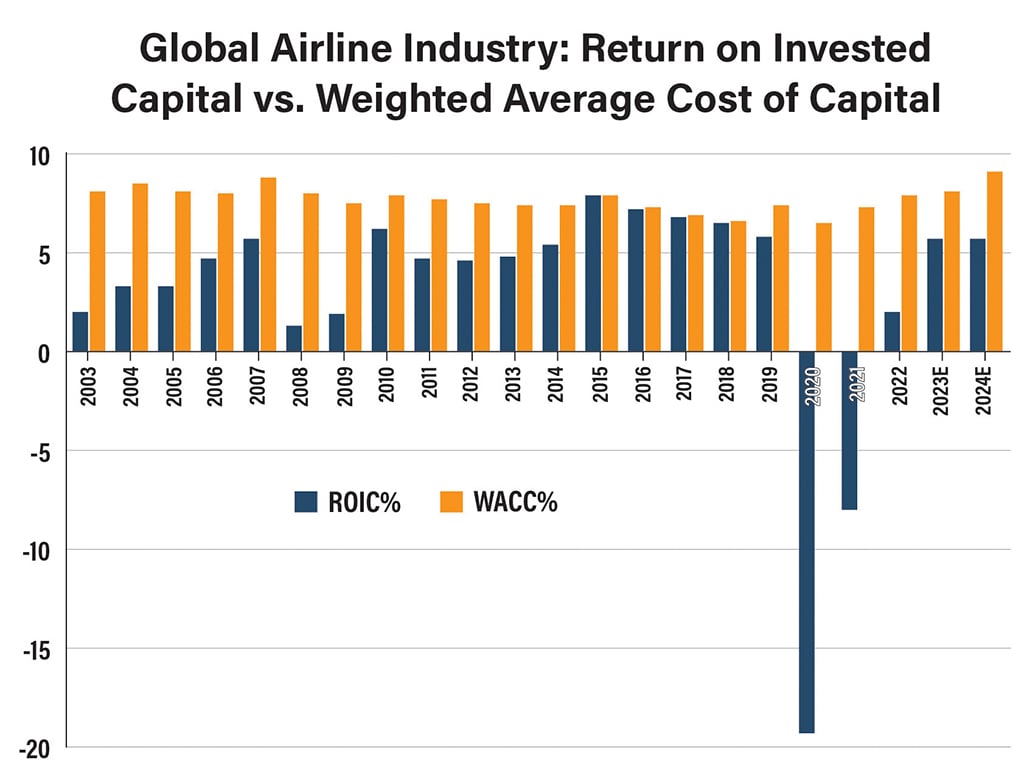

Nevertheless, despite improvements compared with 2019 in almost every measure of traffic, revenue and profits, one crucial indicator is forecast to remain below the level of five years ago. Return on invested capital (ROIC), which measures the profit generated as a percentage of the capital invested in the industry, is not expected to be back to 2019 levels this year.

IATA forecasts ROIC at 5.7% in 2024, just below 2019’s 5.8%. The gap to 2019 is not very significant, but crucially, the gap to the weighted average cost of capital (WACC) is still large. IATA estimates that 2024 ROIC will be about 3.4 ppts below the world airline industry’s WACC, which implies a WACC of 9.1%.

The WACC is the minimum level of return demanded by investors. Since capital is a scarce resource, investors will seek better returns from another sector if returns fail to meet this required minimum.

The weighted average cost of capital takes account of both equity and debt capital and a level of return that takes account of the risk of investing in the sector. Since the COVID-19 pandemic, the cost of debt has risen, and this has contributed to a rise in the WACC.

Meeting its cost of capital has long been a challenge for the airline industry. Even in that unprecedented decade of 10 straight years of positive net profits (2010 to 2019), ROIC levels were not good enough. During that period, ROIC only just about equalled WACC in four years: 2015 to 2018.

A fluctuating measure, the WACC for the global airline industry has varied in the approximate range of 7-10% over the past two decades. However, ROIC has typically fallen short.

It is by no means easy to see the industry regularly exceeding its WACC in the near- to medium term without changes to industry structure. Higher returns are necessary to attract investors to finance the transition to a sustainable future for aviation.

Weak returns reflect a fragmented industry structure in much of the global airline sector. Much of this is because of the high barriers to exit, created largely by governments and regulators. Greater consolidation would improve returns, but this requires policies that are more conducive to consolidation.

Related Content